The History of Blockchain

Introduction

Blockchain technology might seem like a modern innovation, but its origins date back a few decades. This technology has evolved step-by-step, slowly reshaping how we think about trust, money, and information. In this article, we’ll take a journey through the history of blockchain – from its early roots to the rise of Bitcoin, and beyond.

1. The Idea: The Early Roots (1990s)

Long before Bitcoin came into the picture, the idea of a secure digital ledger was already being explored by researchers. In 1991, two computer scientists, Stuart Haber and W. Scott Stornetta, laid the foundation for what would become blockchain technology.

- They were trying to prevent documents from being tampered with.

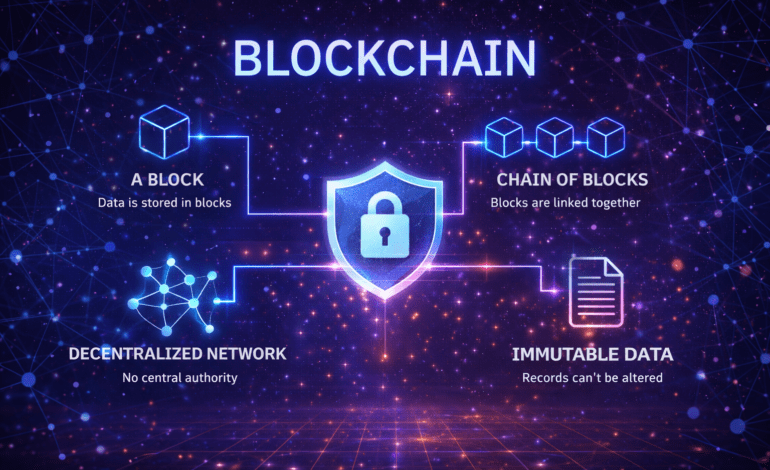

- They proposed a cryptographically secured chain of blocks where each block was timestamped and linked to the previous one.

- This concept ensured that once data was added, it couldn’t be changed or altered.

Although their work didn’t get much attention at the time, it was a critical first step in the development of blockchain technology.

2. Early Digital Currencies: The Late 1990s – 2000s

Before Bitcoin, there were several attempts to create digital currencies. However, most of them failed because they relied on central authorities to manage the currency or were vulnerable to fraud. Some examples include:

- DigiCash (1990s): Founded by cryptographer David Chaum, it aimed to provide private, digital cash but eventually went bankrupt.

- e-gold (1996): This was an attempt to create a gold-backed digital currency but ran into legal trouble and was shut down.

- B-Money and Bit Gold (1998-2005): These were conceptual ideas for decentralized digital money proposed by Wei Dai and Nick Szabo, respectively. Although they were never implemented, their ideas inspired later projects like Bitcoin.

The key problem with these early projects was the “double-spending issue”—if someone could copy digital money, they could use it multiple times. Solving this issue became critical in the development of blockchain.

3. The Birth of Bitcoin: 2008 – 2009

In 2008, an anonymous person (or group) using the name Satoshi Nakamoto released a whitepaper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” This paper introduced Bitcoin, the first decentralized cryptocurrency, and blockchain as the technology that powers it.

What made Bitcoin special?

- Blockchain technology solved the double-spending problem.

- Instead of relying on a bank, transactions were verified by a decentralized network of computers.

- Every transaction was recorded on a public ledger, which was available for everyone to see. Once a transaction was added to the blockchain, it couldn’t be changed or deleted.

In January 2009, Nakamoto released the Bitcoin software and mined the first block, known as the Genesis Block. This marked the beginning of the blockchain revolution.

4. The Rise of Bitcoin and Blockchain: 2010 – 2014

At first, Bitcoin was only known to a small group of tech enthusiasts. But over time, it gained attention as people saw it as a way to send money without banks or governments.

In 2010, Bitcoin made history with its first real-world transaction: a programmer named Laszlo Hanyecz bought two pizzas for 10,000 Bitcoins (now worth millions of dollars). This moment showed that Bitcoin could be used as a form of money.

During these years, people started to realize that blockchain wasn’t just about Bitcoin. Developers began to explore how blockchain technology could be used beyond cryptocurrencies.

5. Ethereum and Smart Contracts: 2015 – 2017

In 2015, Vitalik Buterin, a young programmer, launched Ethereum, a new blockchain platform that introduced the concept of smart contracts.

- A smart contract is a self-executing contract with rules written in code. When certain conditions are met, the contract automatically completes the agreed action.

- Example: If Alice sends money to Bob for a service, the payment is released automatically once the service is delivered.

Ethereum opened the door to decentralized applications (DApps), allowing developers to build applications on the blockchain without relying on centralized servers. This led to the rise of Decentralized Finance (DeFi), Non-Fungible Tokens (NFTs), and other blockchain-based innovations.

6. The Blockchain Boom: 2018 – 2020

As cryptocurrencies became more popular, blockchain technology started gaining mainstream attention. Many companies and industries began exploring how blockchain could improve their operations. Some notable events include:

- IBM, Microsoft, and other tech giants developed private blockchains for supply chain management, finance, and healthcare.

- Governments began exploring the idea of Central Bank Digital Currencies (CBDCs), using blockchain to create state-backed digital money.

- Cryptocurrency exchanges like Binance and Coinbase made it easy for people to buy and trade cryptocurrencies, driving further adoption.

7. Challenges and Criticism of Blockchain

While blockchain technology offers many benefits, it hasn’t been without its challenges. Some of the major concerns include:

- Scalability Issues: As more people use blockchains, networks like Bitcoin and Ethereum became slower and more expensive to use.

- Energy Consumption: Bitcoin’s Proof of Work (PoW) mechanism uses a lot of electricity, raising environmental concerns.

- Regulatory Challenges: Many governments are still figuring out how to regulate cryptocurrencies and blockchain applications.

Despite these challenges, developers are working on solutions, such as Ethereum 2.0 and Layer 2 solutions, to make blockchain networks faster and more energy efficient.

8. The Future of Blockchain: 2021 and Beyond

Blockchain is still evolving, and we are just beginning to see its full potential. Some future trends include:

- Web3: The idea of a decentralized internet where users control their own data.

- Interoperability: Projects like Polkadot and Cosmos are working to connect different blockchains, making it easier for them to work together.

- Governments and Blockchain: Countries like China and the European Union are actively exploring CBDCs, while others are developing blockchain solutions for elections and public services.

As blockchain technology continues to grow, it’s becoming clear that it has applications far beyond cryptocurrencies. From healthcare to supply chain management, blockchain is changing how we think about trust, transparency, and ownership in the digital world.

In Summary

The history of blockchain is a story of innovation, challenges, and constant evolution. What began as an idea to prevent document tampering in the 1990s evolved into Bitcoin, a decentralized currency that sparked a revolution. Today, blockchain is reshaping industries and paving the way for a new digital future.

Blockchain may seem complicated at first, but at its heart, it’s about trust and transparency. As the technology continues to evolve, it will likely play a key role in how we exchange value, share information, and interact online.

We’re only just beginning to explore the potential of blockchain, and the journey promises to be as exciting as the history that brought us here.