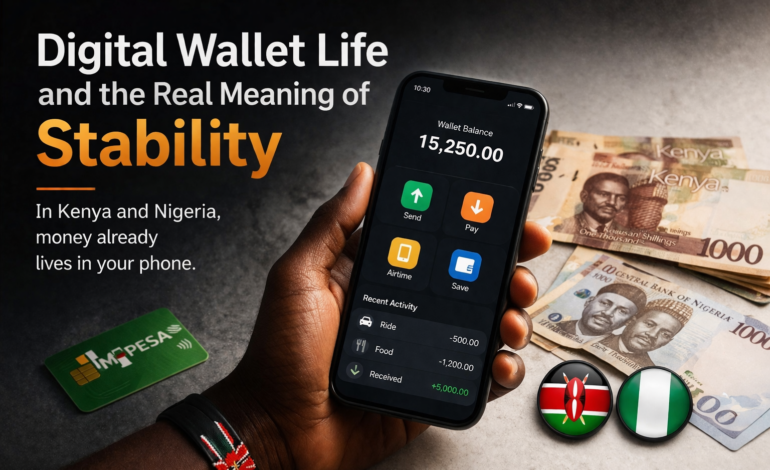

Digital Wallet Life, and the Real Meaning of Stability

In Kenya and Nigeria, money already lives in your phone. You do not need to be persuaded that e

wallets work. You use them to pay for rides, airtime, food, school costs, a supplier, a relative in another

town, and the small everyday transactions that keep life moving. The habit is there. The simplicity is

there. The expectation is there.

So when people talk about “adoption”, it often sounds slightly out of touch. The real question is not

whether people will use a wallet. The question is what kind of money should sit inside the wallet that

people already trust.

In Nairobi, you might do ten small payments before lunch. In Lagos, you might get paid for a job and

immediately think, not in theory but in practice: what do I keep, what do I convert, what do I move, and

how quickly, so tomorrow does not cost more than today.

That instinct is not speculative. It is self defence.

People are not chasing dollars, they are chasing stable purchasing power

When someone says, “I’m moving into dollars,” it is rarely about admiration for the United States. It is

about something more basic. They want their money to keep its meaning.

Local currencies are asked to carry a heavy load. Import dependence, commodity shocks, policy

mistakes, and global interest cycles show up in the price of essentials. When inflation rises, it does not

arrive as a headline. It arrives as stress.

Sometimes inflation becomes something worse. Hyperinflation is not simply prices going up. It is when

prices stop behaving. Merchants reprice constantly. Salaries lose meaning. People stop saving because

holding cash becomes a guaranteed loss. When money breaks like that, it takes trust down with it.

So people adapt. They buy earlier. They hold goods. They store value in whatever is most accessible.

Why the real dollar can be strangely out of reach

In theory, anyone can hold USD. In practice, access is uneven. Banking rules, account minimums, limits,

delays, and sudden changes in what is “allowed” can make dollars feel like a privilege rather than a

normal tool. Physical cash dollars can be expensive to obtain, risky to keep, and awkward to move.

This gap between what is possible and what is practical is where USD stablecoins found their place.

Why USD stablecoins feel like the smartest option on the table

Stablecoins turned the dollar into something phone native. That matters in places where people already

trust digital money. A digital dollar is easy to grasp, easy to price, easy to compare, and often easier to

move than bank dollars.

For many users, stablecoins have been a genuine upgrade.

But there is a gentle truth worth naming early, because it will guide this series.

A dollar peg is not the same as stable purchasing power. The number might stay stable, but the dollar

itself changes over time. And because the dollar is a national currency, its policy cycle is ultimately

shaped by what the United States needs at home. That is not a moral judgement. It is simply how

national currencies work.

If your goal is purchasing power, the peg can be a useful bridge, but it may not be the final destination.

In the next article we will look at the moment this difference becomes visible. Not when you hold, but

when you use. Not the peg, but the pathway.