The Least Unstable Option: Why Africa’s Crypto Laboratory Should Consider Alternatives to Dollar Stablecoins

Africa has quietly become one of the world’s largest real-world crypto laboratories. Not Silicon Valley, not Wall Street, and not even Switzerland, but cities like Nairobi, Lagos, Accra, Cape Town, and Kigali.

Here, crypto has moved far beyond conference halls and trading speculation. It operates in markets, WhatsApp groups, remittance corridors, and daily survival strategies. For millions of Africans, crypto is no longer an investment. It is infrastructure.

Recent data confirms this shift. According to Binance Research in 2026, emerging markets now account for 77% of the platform’s users, up from 49% in 2020. Roughly 73% of stablecoin savers on the platform are in these economies, with 36% of emerging market users holding more than half their portfolios in stablecoins.

Within this ecosystem, one asset dominates: USDT (Tether). It has become the digital dollar of Africa’s street economy, used by freelancers for payments, importers for value preservation, traders for hedging, and families for remittances. In high-inflation environments, young Africans increasingly store wealth in it.

USDT functions as Africa’s unofficial reserve currency in practice. But its dominance raises a deeper question: If the goal is genuine stability, why do we default exclusively to the US Dollar when other currencies have historically shown stronger long-term purchasing power preservation, such as the Swiss Franc?

Stability Is Relative

Most Africans adopt USDT not out of love for the US Dollar, but because local alternatives are worse. When national currencies lose value rapidly, even a moderately inflationary dollar appears stable by comparison. People fleeing monetary chaos seek shelter, not perfection.

Dollar stablecoins succeeded by offering speed, accessibility, and relative predictability where traditional systems failed. A smartphone and internet connection now provide access to global financial rails.

Yet USDT carries a built-in limitation: its stability is relative. Over decades, the US Dollar itself erodes purchasing power through inflation. What feels reliable year-to-year looks less impressive over 20–50 years. This is not unique to the dollar, nearly all fiat currencies face gradual debasement, but it highlights a core truth: many users are choosing the least unstable option available, not ideal stability.

The Swiss Franc’s Track Record

For decades, the Swiss Franc earned a reputation for monetary restraint, supported by Switzerland’s political neutrality, conservative fiscal policies, and strong institutions. During global crises, capital has often flowed into the CHF as a safe haven.

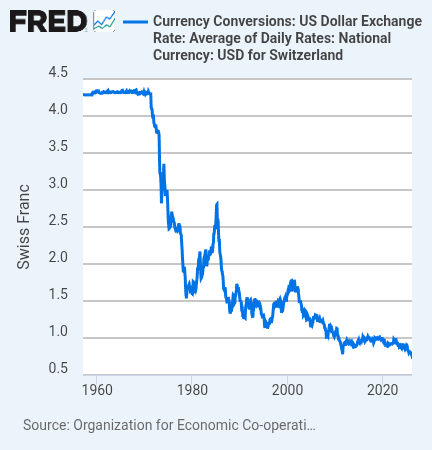

The numbers illustrate this resilience. In the early 1970s, it took roughly 4.3 Swiss Francs to buy one US Dollar. By mid-2026, the rate had fallen to around 0.78–0.79 CHF per USD, a substantial nominal appreciation of the franc. While both currencies have lost purchasing power over time, Switzerland has generally maintained lower cumulative inflation, especially during high-inflation periods like the 1970s.

This is not “perfect money.” The Swiss Franc has also depreciated in real terms over generations. However, its relative strength matters for long-term savers.

Switzerland’s success stems not only from policy but from geopolitics, deep financial integration, and accumulated institutional trust, factors difficult to replicate quickly.

Crypto’s Central Contradiction

Bitcoin launched after the 2008 crisis as a challenge to centralized monetary systems. Yet much of today’s crypto ecosystem runs on dollar-backed stablecoins. The industry sought to escape traditional finance but rebuilt versions of it using US Treasuries and dollar reserves for credibility.

Switzerland has taken a more integrative approach, using regulatory clarity to embed digital assets into its system rather than treating them as pure disruption. This raises a useful contrast: crypto often prioritizes speed and decentralization, while Swiss finance has historically optimized for continuity and survivability.

The Thought Experiment: A CHF Stablecoin

Imagine a liquid, well-regulated Swiss Franc stablecoin operating at global scale, fully backed, redeemable, and accessible via blockchain. Historically, it could preserve purchasing power better over decades than pure USD equivalents.

However, significant barriers exist. The US Dollar benefits from overwhelming network effects: it prices commodities, dominates trade settlement, sovereign reserves, and global banking rails. Liquidity attracts more liquidity. Adoption frequently beats theoretical optimization. Existing small CHF stablecoins like XCHF demonstrate technical feasibility, and in 2026 major Swiss banks (including UBS) launched a sandbox to test broader CHF stablecoin use cases,but scaling to African street-level utility remains a steep challenge.

Practical hurdles for African users include limited on/off-ramps, higher friction, potential FX volatility when converting to local needs, and lower liquidity compared to USDT.

Why Africa May Ask These Questions First

Africa experiences monetary instability more acutely than most regions. Inflation is not abstract, it appears in rising food prices, school fees, and eroding savings. This lived reality makes Africans pragmatic experimenters.

USDT adoption has solved urgent problems, particularly in places like Nigeria. Yet the long-term conversation should evolve. A multi-wallet future makes sense: using dollar stablecoins for transactions and liquidity, while allocating savings to stronger-preserving assets like a CHF-backed option where feasible. This layered approach could better balance utility and preservation.

The Deeper Lesson

Africa should not try to imitate Switzerland. The continent’s younger population, faster-growing economies, and unique developmental needs demand tailored solutions.

The real lesson is about trust and institutions. Technology alone cannot create stable money. Blockchain enhances transparency and efficiency, but credible governance and monetary foundations remain essential. Trust compounds slowly over generations, something the Swiss Franc exemplifies.

Africa’s crypto laboratory is already testing what “stable money” truly means in the digital age. The next evolution may involve moving beyond settling for the least unstable option toward more sophisticated, multi-currency strategies that better serve both daily needs and long-term preservation.

True stability, after all, survives crises while protecting confidence over time.