The Evolution of Money: From Barter Systems to M-Pesa and Cryptocurrency

Money emerged not as an invention of governments but as a solution to coordination problems in human exchange of value.

Before money, trade relied on barter. It worked,but couldn’t scale – it was limiting.

Early-ish human societies, trade was direct and personal. One person had cereal, another had livestock. All that was needed was alignment,then exchange happened. But this system ,simple and direct, depended on what economists could later describe as the double coincidence of wants: both parties needed to want exactly what the other offered, at the same time, and in the right quantity.

A bottle neck that needed to be solved and money emerged as a solution to this coordination problem.

Money as a Tool for Trust

Money is not defined by the forms it is represented.Whether shells, metal, paper, or digital entries, money functions because collective persons agree it can represent value, facilitate exchange, and store purchasing power.

Early forms of money reflected local realities. Cowrie shells circulated across parts of Africa and Asia. Salt functioned as currency in the Roman world.But with time, precious metals gained prominence because they were scarce, durable, divisible, and widely accepted. Over time, states standardized money through coinage, the Spanish piece of eight is a good example here,stamping authority onto units of value to reduce disputes and build trust.

Paper money followed, initially representing claims on assets ( Precious metals ) held by trusted institutions. Eventually, most economies moved to fiat systems, where currency is backed not by a physical commodity but by government authority and institutional credibility. The earliest form of a national fiat backed system was introduced by Kublai Khan in the 13th century.

Every shift shared a common goal: reduce friction, expand trade, preserve value better and enable trust at a bigger scale.

Global Financial System with Uneven Access

Today, money is largely digital. Bank balances exist as ledger entries. Payments move through clearing systems, correspondent banks, and central bank infrastructure. Yet access to these systems remains unequal,gatekept and costly to many in Africa.

In many developed economies, financial inclusion is assumed. In large parts of the Global South, including Africa, millions have historically operated on the margins of formal banking ,despite being economically active. This gap created space for alternative monetary innovations.

Kenya: When Money Adapted to Reality

Kenya’s experience illustrates how money evolves when traditional systems fail to meet everyday needs.

Before mobile money, banking access was limited, transaction costs were high, and physical branches were sparse. Yet informal trade, savings groups, and remittances formed the backbone of economic life.

The launch of M-Pesa in 2007 changed the trajectory. A mobile phone number became a financial identity. SMS became a payment rail. Trust shifted from bank counters to a digital ledger backed by a telecom network.

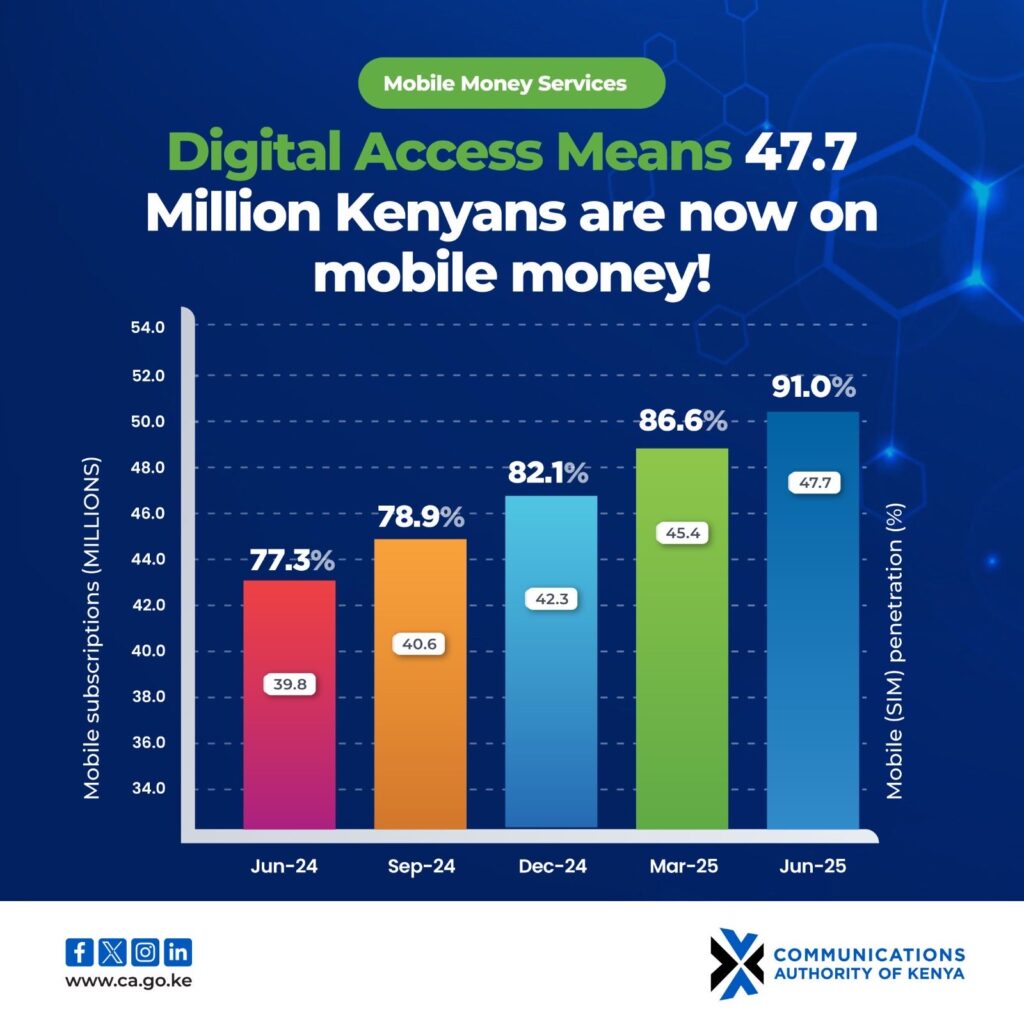

Today, over 90% of Kenyan adults use mobile money as per the Communication Authority of Kenya report, making it a central layer of the economy rather than a parallel system. It supports household payments, small businesses, transport, and emergency transfers. Kenya demonstrated that money does not need to look like a bank to perform banking functions.

However, mobile money also revealed limitations. These systems are centrally controlled, largely closed, and constrained by national borders. Cross-border payments remain costly, and integration with global digital markets is limited.

Crypto: Rethinking How Value Moves

M-Pesa did not just digitize payments;it redefined who could participate in financial infrastructure by moving trust from banks to telecom networks. Crypto is introducing an alternative model of monetary issuance challenging the traditional role of central banks as sole issuers of currency.

As F.A. Hayek, a British economist suggested, money shouldn’t be a government monopoly; it should be a choice. For Kenya, crypto, is about solving three specific problems:

- Sending Money Home (Remittances): Currently, sending money from the UK or US to Kenya often involves “middleman” fees that eat up a significant chunk of the transfer. Crypto moves fast, bypassing the 3–5 day waiting period of traditional wire transfers.Remittances via stablecoins cut costs sharply (often to <1% vs. 6-8% traditional), and adoption continues growing

- Beating Inflation with Stablecoins: We’ve all felt the Shilling’s fluctuations. Stablecoins (digital tokens pegged to the US Dollar) allow a trader in Eastleigh to “hold” value in a stable currency on their phone, without needing a formal USD bank account which is often hard and costly to open.

- The Power of Programmable Money: Imagine a “Chama” (savings group) where the rules are written in code. No one can “disappear” with the funds because the smart contract only releases money when the group’s conditions are met. This is trust, but automated.

The Bridge:Stablecoins

For many users, crypto feels too volatile,like a roller coaster. But Stablecoins appear to bridge speed and borderless nature of crypto but with the price stability of the Dollar ,Euro or Gauge cash. They represent the “M-Pesa-fication” of global currency; easy to move, easy to track, and accessible to anyone with a smartphone.

Continuity, Not Disruption for Its Own Sake

Money has never been static. From barter to coins, paper, bank ledgers, mobile wallets, and now blockchains, each evolution has layered new capabilities onto existing systems.

Crypto challenges long-standing assumptions about who can issue money, how trust is coordinated, and how value flows across borders.

As governments debate and legislate on digital assets and as blockchain-based payment rails mature, these questions are not an afterthought. For Kenya and other emerging economies, the opportunity lies in shaping how these tools are adopted and grounded in real economic needs.

Whether crypto becomes dominant or simply another layer in the evolution of money remains uncertain,but its emergence signals that the architecture of trust itself is being renegotiated.

Because money, in every era, reflects how societies choose to trade, coordinate, and build value at large.