The $1 Trillion Harvest: Why Africa’s Next Financial Revolution Will Be Built on Crops, Not Code

Let’s start with a number that should make every builder, investor, and policymaker in Africa sit up straight.

Africa’s agricultural sector is worth over $1 trillion. The continent holds 60% of the world’s uncultivated arable land. Agriculture employs more than half of sub-Saharan Africa’s workforce. Smallholder farmers produce over 70% of the food.

And yet. AND YET.

These farmers, the people who literally feed the continent, are among the most financially excluded humans on the planet. They can’t get bank loans because they have “no collateral.” They sell their harvest at rock-bottom prices because they can’t afford to store it. They borrow from informal lenders at rates that would make a Sumerian temple priest blush.

Here’s the thing, though. This problem? It was solved before. About 4,000 years ago.

(If you’re just joining, this is the follow-up to my previous piece where I started diving into this rabbit hole.)

The Ancient Playbook

I’m not going to make you sit through a history lecture. But I need you to understand three things, because they’re the foundation of everything that follows.

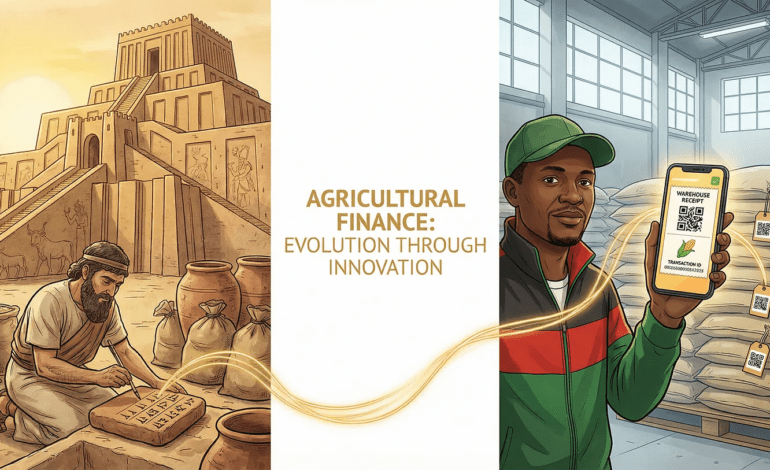

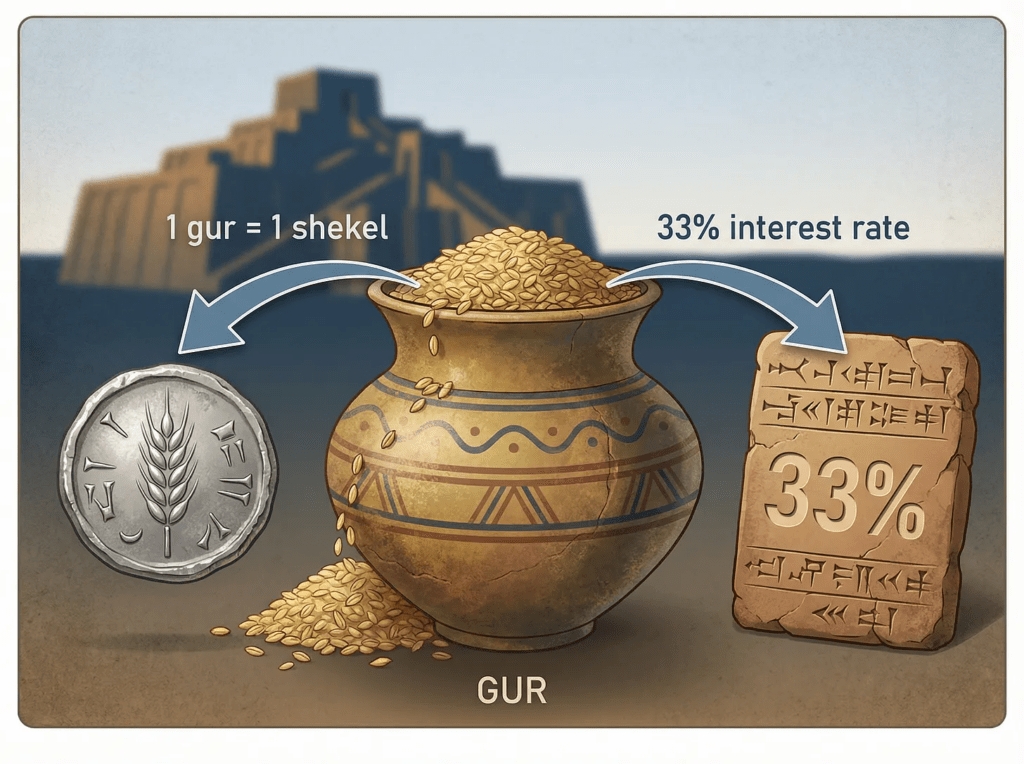

1: Barley Was Money

In ancient Mesopotamia (modern Iraq), the economy ran on barley. One gur of barley, about 300 litres, was worth one shekel of silver. This wasn’t a suggestion. It was the state-regulated exchange rate that governed all wages, taxes, and trade.

Temples functioned as banks. They stored grain, recorded deposits on clay tablets, and issued interest-bearing loans at 33% for barley and 20% for silver. That 33% rate accounted for the seasonal price drop after harvest, built-in inflation adjustment, 4,000 years before central bankers invented the term.

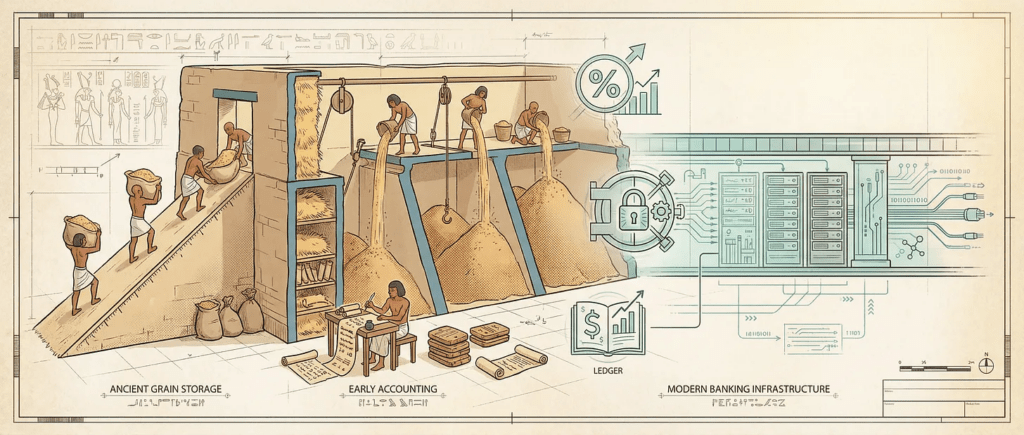

2: Grain Storage = Banking

Tate Paulette at the University of Chicago studied ancient Mesopotamian grain silos and concluded: “Grain was king. Or, to put it more accurately, grain made kings”.

The silo was the bank vault. The clay tablet was the bank statement. The temple accountant was the loan officer. The entire financial system was built on stored agricultural output.

Egypt did the same thing with wheat, paying pyramid workers in bread and beer, running state warehouses where farmers could deposit grain and draw against it. Their grain loans charged up to 100% interest. (Even Kenya’s SACCOs aren’t that bold.)

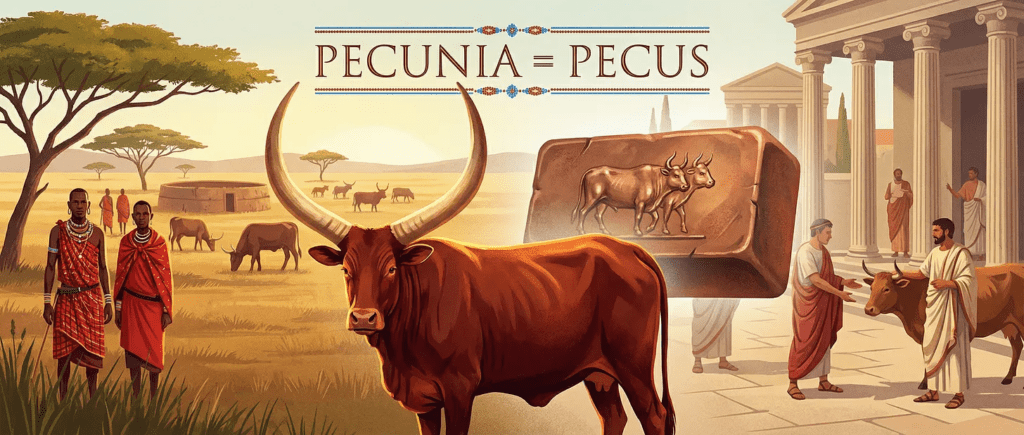

3: Cattle Was the Original $$$

In Rome, the word for money, pecunia, literally means cattle. Fines were paid in livestock. State wealth was measured in herds. The crime of embezzling public funds was called peculatus: cattle theft.

Across pre-colonial East Africa, the same was true. Among the Akamba: “cattle was an accepted measure for evaluating wealth… a unit of accounting against which the value of prestige goods, like hoes or cloth, was measured”. In Buganda, currencies evolved through barkcloth, beads, ivory discs, and cowrie shells, with cattle always holding a special place as the ultimate store of value.

Colonialism replaced these systems with imported currencies. But the logic, productive assets as money, persisted in how communities actually thought about wealth.

What Broke (And What’s Being Fixed)

Ancient grain money had three problems: it was heavy, it rotted, and its price swung with the weather. Silver and gold solved those problems but introduced new ones, mainly that money became disconnected from productive reality.

Fast forward a few thousand years and we have fiat currencies backed by government promises, financial instruments backed by other financial instruments, and a global system that produced 425 systemic crises between 1970 and 2010. That’s more than 10 per year.

Meanwhile, in Kenya, a farmer with 100 bags of stored maize, a commodity with real, intrinsic value, can’t get a loan because banks say she has “no recognised collateral.”

The ancient Sumerians would find this genuinely baffling. Their entire banking system was built on the premise that grain IS collateral. The most creditworthy thing in the world is food.

Here’s what’s changing:

Kenya’s e-WRS: The Grain Bank Reborn

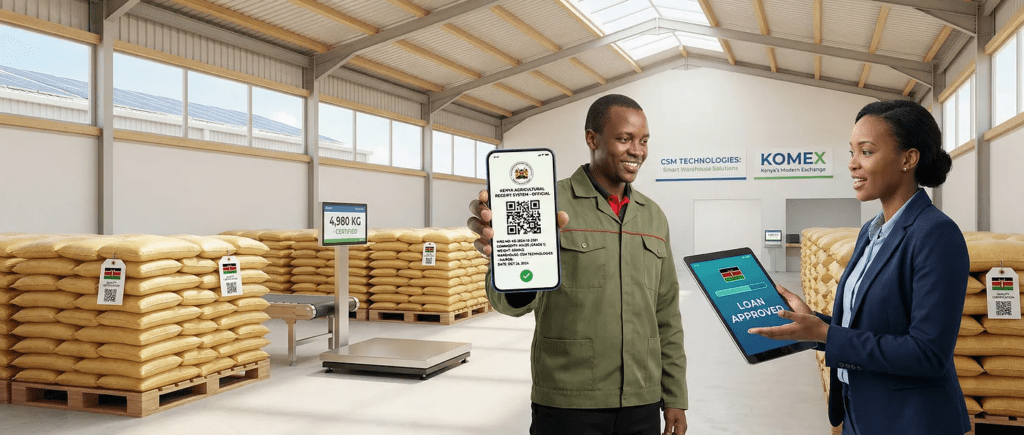

February 25, 2026. Kenya launches its electronic Warehouse Receipt System. Let’s break down exactly what this means.

Before e-WRS: A farmer harvests maize. Has two options: (a) sell immediately to middlemen at harvest-time prices, or (b) store at home where weevils, moisture, and theft eat away at the value. Either way, they can’t access formal credit because banks won’t accept grain as collateral.

After e-WRS: Farmer deposits maize in a certified warehouse. Gets an electronic receipt, a legally binding digital document integrated with the national ID system and KRA. Takes that receipt to a bank. Bank says: “We see you have 600,000 shillings worth of certified maize. Here’s a loan.” Farmer uses the loan for seeds, school fees, or investment. Sells the maize three months later when prices have risen 20%. Repays the loan. Keeps the profit.

That’s not theory. 114 receipts have already been issued. 44% have been used to access financing.

This is the Egyptian grain bank, digitised, regulated, and integrated with Kenya’s financial infrastructure. The grain stays in the warehouse. The value moves on the network.

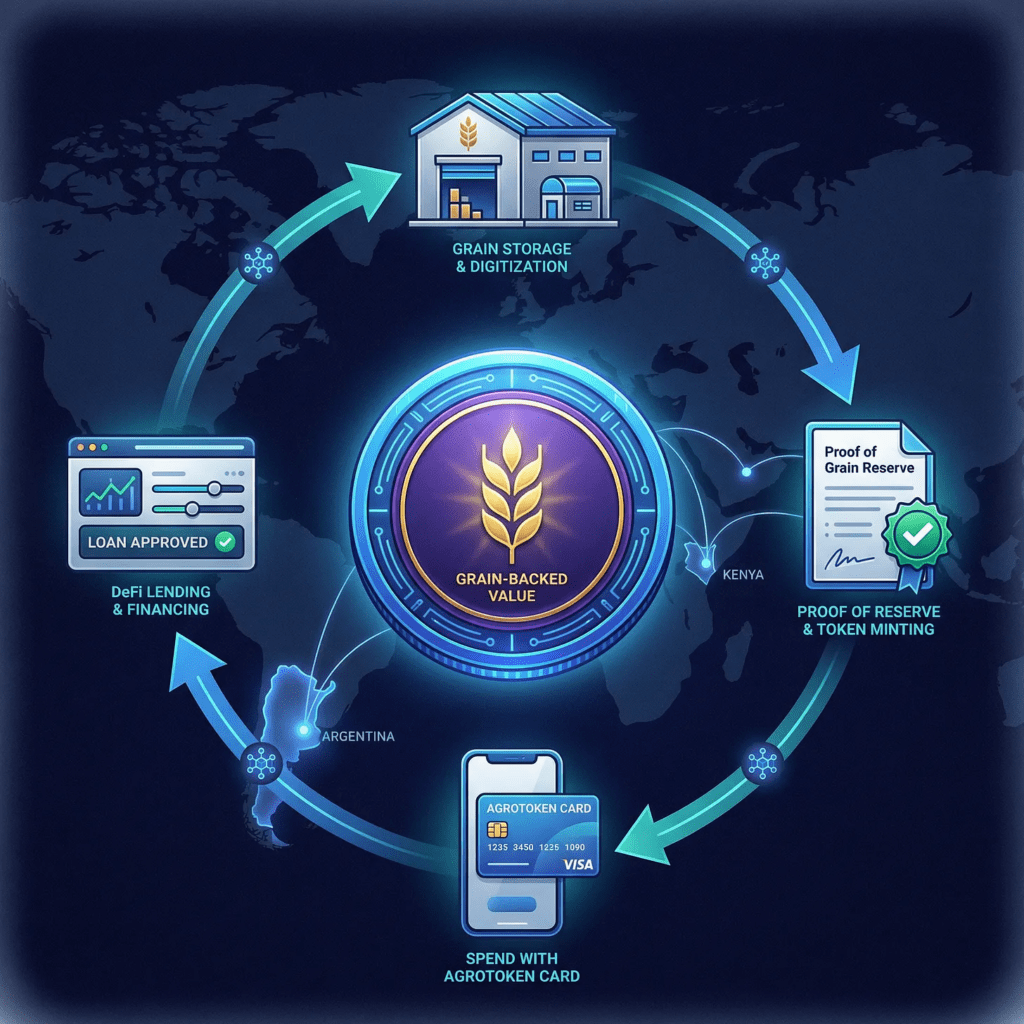

Agrotoken: Proof This Model Scales

In Argentina, Agrotoken has turned this exact concept into a blockchain-native product. One token = one ton of grain. The grain sits in a warehouse. A “Proof of Grain Reserve” certificate backs the token. In 2022, Santander started accepting Agrotokens as loan collateral, “the first global experience in backing loans with tokens related to agricultural commodities”.

They’ve also partnered with Visa, so farmers can spend their grain tokens with a payment card. Think about that, a farmer’s harvest, tokenized, sitting on a blockchain, spendable at any Visa terminal in the world.

Kenya’s e-WRS is the foundation. Agrotoken is the proof of concept. The question is: who builds the African version?

Three Things That Could Be Built Tomorrow

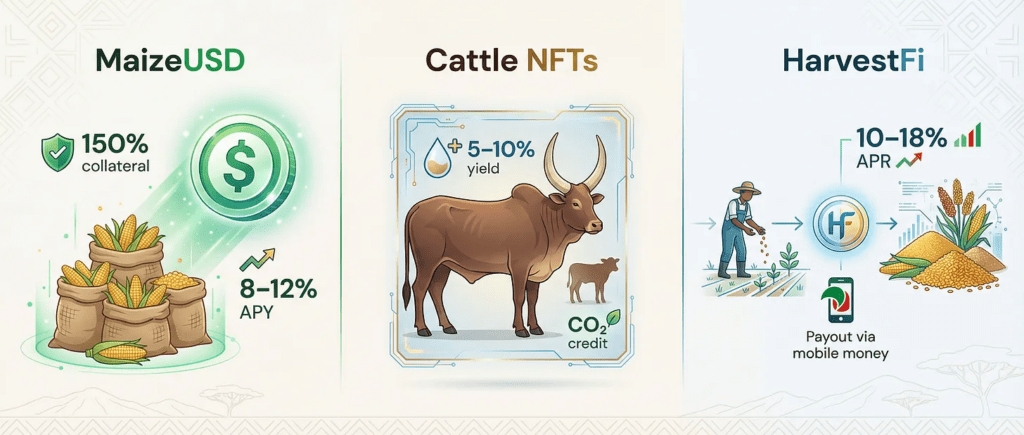

1. A Maize-Backed Stablecoin

A dollar-pegged stablecoin over-collateralized by tokenized maize from Kenya’s e-WRS warehouses. 150% collateral ratio. Oracle price feeds from KOMEX. Weather-indexed insurance for climate risk. Yield from seasonal price appreciation (maize typically rises 15 to 30% from harvest to pre-harvest) plus DeFi lending income. Target: 8 to 12% annualized yield.

This isn’t science fiction. Every component exists today. The e-WRS provides legally recognised digital receipts. DeFi protocols like Aave and Compound (and their forks) provide lending infrastructure. Chainlink provides price oracles. All that’s missing is someone stitching them together.

2. Tokenized Future Harvests (Pay-Later Seeds)

The ancient Sumerians lent barley to farmers before harvest and collected repayment after. The modern version: farmers mint tokens representing projected harvests, sell them to investors at a discount, use the capital for inputs, and deliver grain at harvest for redemption.

One Acre Fund already does a version of this with M-Pesa-linked loan repayments, their farmers earn 48% more than peers. Add tokenization and you open this up to global capital markets. A yield investor in Singapore funding a maize harvest in Nyandarua, settled in stablecoins, verified by satellite crop monitoring.

3. Cattle Yield NFTs

Each NFT = one verified head of cattle in a registered dairy cooperative. Yield from milk revenue, calf births (the ancient Romans called this “calf-interest,” it was literally the origin of the concept of interest), and carbon credits from regenerative grazing. Quarterly distribution via smart contract.

This is what my team and I are building at Project Mocha, tokenizing 2,000 geotagged coffee trees in Embu, where token holders fund farm rehabilitation and receive their ROI from the sold coffee harvests. The model works. It just needs to be replicated across crops and livestock.

The Regulatory Window Is Open

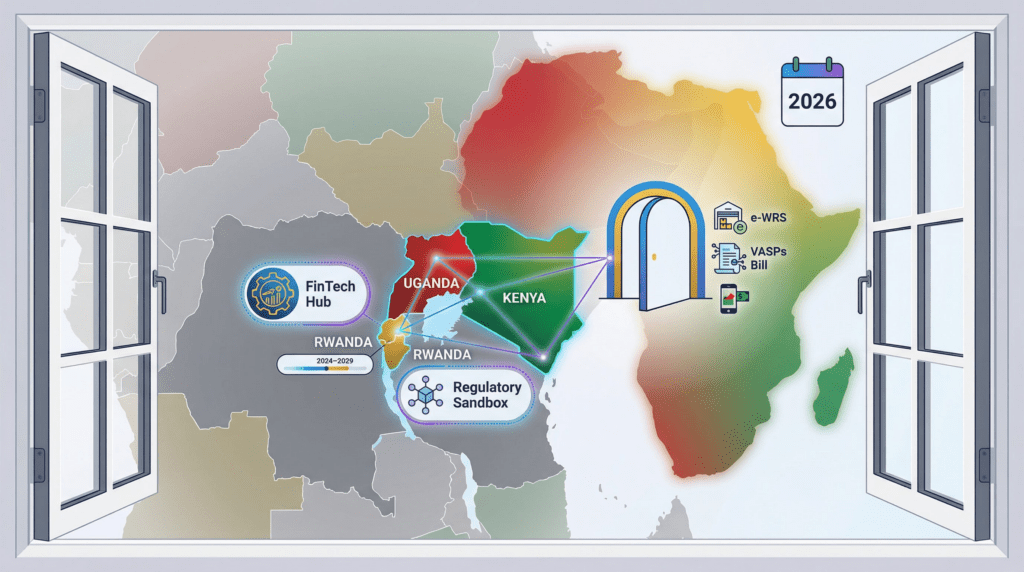

This isn’t a “wait for regulators” situation. The window is open now.

Kenya: The e-WRS is government-backed infrastructure. The VASPs regulatory framework is in development after been passed into law in late 2025. The CMA has a regulatory sandbox. M-Pesa provides last mile rails for instant on-ramp/off-ramp.

Rwanda: Actively positioning itself as Africa’s fintech hub with its 2024 to 2029 FinTech Strategy and RURA sandbox.

Uganda: Bank of Uganda’s regulatory sandbox is operational and explicitly open to blockchain experiments.

The pioneers who build in this window, with compliance baked in from day one, will set the standard for the continent.

Why You Should Care

Here’s the big idea, distilled:

For 8,000 years, money was backed by productive output. Grain, cattle, harvests, real things that sustained real people. Then we switched to abstract money backed by government promises. The results have been… mixed. (425 systemic crises in 40 years. Billions of people financially excluded. Inflation eating savings.)

Africa has the agricultural output, the mobile infrastructure, the young builders, and the regulatory openness to bring money back to its productive roots. Not as a regression, as an upgrade. Ancient logic, modern tools.

A farmer in Nakuru deposits maize in a warehouse. Gets a digital receipt. Mints a stablecoin. Lends it on a DeFi protocol. Earns yield while waiting for prices to rise. Sells at the optimal time. Repays the loan via M-Pesa. All of this verified, transparent, composable.

That sequence has an ancient precedent in every civilization that preceded ours. The Sumerians, the Egyptians, the Romans, the pre-colonial Akamba, they all understood that productive output is the most honest form of money.

We just forgot. Africa is about to remember.

Frequently Asked Questions (FAQs)

What is Kenya’s electronic Warehouse Receipt System (e-WRS)?

Kenya’s electronic Warehouse Receipt System (e-WRS) allows farmers to deposit crops such as maize in certified warehouses and receive a digital receipt representing the stored commodity. This receipt is legally recognized and can be used as collateral to access bank loans. Instead of selling crops immediately after harvest when prices are low, farmers can store their produce, borrow against it, and sell later when prices rise.

How do warehouse receipts help farmers access financing?

Warehouse receipts act as proof of ownership of stored commodities. When crops are deposited in certified warehouses, farmers receive a receipt that shows the quantity and quality of the stored produce. Banks can accept these receipts as collateral, allowing farmers to secure loans without traditional assets such as land titles or buildings.

What is agricultural tokenization?

Agricultural tokenization is the process of converting real-world agricultural assets, such as grain, coffee, or livestock, into digital tokens on a blockchain. Each token represents ownership or value tied to a physical commodity stored in verified locations such as warehouses or farms.

Tokenization allows agricultural assets to be:

- traded digitally

- used as collateral in decentralized finance (DeFi)

- accessed by global investors

This approach can unlock new financing for farmers and agricultural businesses.

Can blockchain help solve agricultural financing in Africa?

Yes. Blockchain technology can improve agricultural financing by creating transparent, verifiable digital records of real-world assets such as stored crops. When combined with systems like Kenya’s e-WRS, blockchain can allow commodities like maize or coffee to be tokenized and used in decentralized financial systems.

This can enable:

- faster access to credit

- global investment into agriculture

- transparent collateral verification

- programmable financial contracts for farmers

What is a maize-backed stablecoin?

A maize-backed stablecoin is a digital currency whose value is backed by stored maize or maize warehouse receipts. Instead of being pegged to a fiat currency like the US dollar, the stablecoin is collateralized by agricultural commodities.

For example:

- maize stored in certified warehouses is verified

- digital tokens are issued representing that maize

- those tokens can support a stablecoin used in DeFi or payments

This concept combines commodity finance and blockchain technology.

What are tokenized agricultural assets?

Tokenized agricultural assets are digital representations of real-world farm products or resources. These can include:

- grain stored in warehouses

- livestock such as cattle

- coffee trees or plantations

- future harvest yields

Tokenization allows these assets to be fractionally owned, traded globally, and used in financial markets.

Why are African farmers often excluded from traditional banking?

Many African farmers cannot access bank loans because they lack formal collateral recognized by financial institutions. Banks often require assets such as land titles, buildings, or registered businesses.

Smallholder farmers may instead hold wealth in:

- crops

- livestock

- future harvests

Systems like warehouse receipts and tokenized commodities help convert these productive assets into recognized financial collateral.

What are real-world assets (RWAs) in blockchain?

Real-world assets (RWAs) are physical assets that are represented on a blockchain through digital tokens. Examples include real estate, commodities, bonds, or agricultural products.

In agriculture, RWAs could include:

- stored grain

- coffee harvests

- cattle herds

- farmland production

Tokenizing RWAs allows them to participate in decentralized finance (DeFi) and global capital markets.

How could DeFi benefit farmers?

Decentralized finance (DeFi) can provide farmers with new ways to access capital without traditional banks. Through tokenized assets and smart contracts, farmers could:

- borrow against stored crops

- sell future harvests to investors

- receive global funding through blockchain platforms

- earn yield on tokenized commodities

This creates financial opportunities that were previously unavailable to smallholder farmers.

Why is Africa well positioned for agricultural blockchain innovation?

Africa has several advantages that make it suitable for agricultural blockchain systems:

- large agricultural output

- millions of smallholder farmers needing financing

- widespread mobile payment infrastructure like M-Pesa

- emerging regulatory sandboxes for fintech and blockchain

- young technology builders and entrepreneurs

These factors create an environment where tokenized agriculture and digital commodity finance can grow rapidly.

Next time someone tells you crypto has no real-world use case in Africa, send them this article. Then send them a bag of Kenyan Coffee and ask if they now understand collateral .

About me: Peter Maina has spent over a decade taking products from idea to market across AgriTech, fintech, and Web3. As a 2X founder and full-stack marketer & operator, he sees technology not as the destination but as the bridge connecting underserved communities to profitable, meaningful livelihoods