Africa’s Payment Walls Are Cracking: Kenya and Rwanda Take the First Regulatory Step

A new agreement between the Central Bank of Kenya (CBK) and the National Bank of Rwanda (NBR) signals a significant step toward regulatory alignment in Africa’s rapidly expanding digital payments sector.

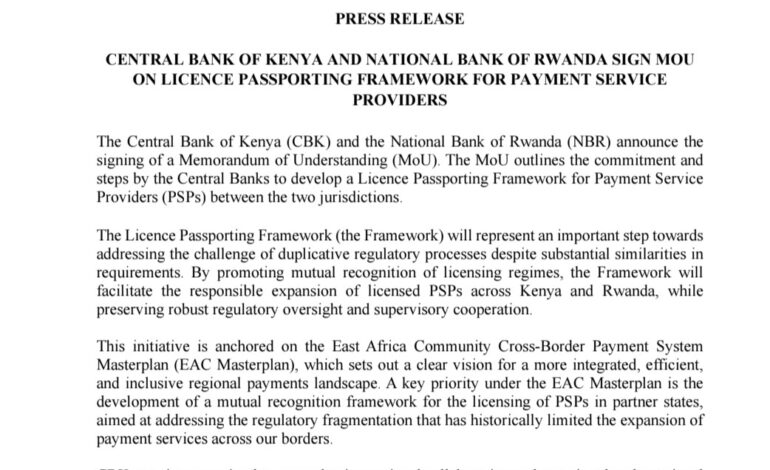

In a press release dated March 11, 2026, the two central banks announced the signing of a Memorandum of Understanding (MoU) to develop a Licence Passporting Framework for Payment Service Providers (PSPs). The agreement aims to allow licensed fintechs, mobile money providers, and digital wallet operators in one country to expand into the other with streamlined regulatory approval.

If successfully implemented, the framework could reduce one of the biggest barriers facing African fintech startups: the need to undergo multiple licensing processes in every new jurisdiction.

A Step Toward Regulatory Harmonization

Under the proposed system, a PSP licensed in Kenya could operate in Rwanda , and vice versa — through a mutual recognition mechanism between the two regulators.

While oversight would remain in place, the passporting model would reduce duplicative regulatory requirements where licensing standards already overlap.The concept mirrors the regulatory “passporting” system used in parts of Europe, where financial institutions can operate across borders under a unified framework.

For East Africa’s fintech ecosystem, the potential implications are substantial. Kenya has long been regarded as a global leader in mobile payments, largely driven by platforms such as M-Pesa, while Rwanda has positioned itself as one of Africa’s most ambitious digital economy hubs.

Together, the two markets offer a compelling test case for cross-border fintech integration.

Anchored in Regional Integration Plans

The MoU is not an isolated initiative. It is explicitly linked to the East African Community Cross-Border Payment System Masterplan, a regional roadmap adopted by central bank governors within the East African Community (EAC).

The Masterplan outlines a five-year strategy focused on:

- Legal and regulatory harmonization

- Modernization of payments infrastructure

- Financial inclusion

- Institutional capacity building

One of its core objectives is mutual recognition of PSP licenses, designed to reduce the regulatory fragmentation that has historically slowed cross-border financial services in the region.

The EAC currently includes Kenya, Rwanda, Uganda, Tanzania, Burundi, South Sudan, the Democratic Republic of Congo, and Somalia.

Despite growing economic integration, payments across these markets often remain slow, expensive, and administratively complex.

Linking to Africa’s Broader Payments Transformation

The Kenya–Rwanda initiative also fits into wider continental reforms.

Africa’s financial integration agenda is being driven in part by the African Continental Free Trade Area (AfCFTA), which seeks to create a unified market of more than 1.4 billion people.

One of the key obstacles to intra-African trade has been the difficulty of making fast and affordable cross-border payments.

To address this, the Pan-African Payment and Settlement System (PAPSS), developed with support from Afreximbank, allows participating banks and financial institutions to settle transactions directly in African currencies.

Simplifying licensing requirements for PSPs could make it easier for fintech platforms to integrate with these emerging payment rails.

Opportunities — and Practical Challenges

For businesses and consumers, the benefits could be substantial.

A functioning passporting system could enable:

- Faster cross-border wallet transfers

- Lower transaction costs for SMEs and traders

- Increased competition among fintech providers

- Greater regional financial inclusion

However, the agreement remains an initial framework rather than an operational system.

Significant technical work remains, including:

- Aligning anti-money laundering (AML) and counter-terror financing standards

- Developing cross-border supervisory protocols

- Establishing consumer protection rules

- Ensuring cybersecurity and data-sharing safeguards

Implementation will be overseen by a joint technical committee, meaning the rollout will likely take time.

A Test Case for Africa’s Fintech Future

While still early, the Kenya–Rwanda initiative represents a broader shift in African financial policy, moving from high-level integration goals to practical regulatory cooperation.

If the model proves effective, similar passporting arrangements could emerge across other African regional blocs, including ECOWAS and SADC.

For now, the agreement reinforces East Africa’s role as one of the continent’s most active fintech laboratories, where regulatory innovation is increasingly keeping pace with technological change.

And if expanded regionally, it could help chip away at one of Africa’s oldest economic barriers: the high cost of moving money across borders.